Acorn is a Time-Driven Activity-Based-Costing (TDABC) platform that distills and attributes costs of delivering products and services by building business-specific models which take into account nuances of account processes. With Acorn, you can also build datamarts (OLAP cubes) to deliver accurate and insightful financial analytics on any business dimension (e.g. product, customer, facility, region, SKU and more).

Measure, Manage and Improve Every Element of Your Business

- Clearly determine your profitable and unprofitable products and understand why

- Access insights to help negotiate better terms with your suppliers and customers

- Build reports and dashboards that drive profitable behavior across regions and facilities

- Develop the right pricing strategy across products and services

- Make accurate decisions relative to your inventory, stock and overall supply chain inputs

UNDERSTAND HOW DECISIONS IMPACT YOUR BOTTOM LINE

- Identify your most profitable customers, channels and products

- Run what-if profitability scenarios across multiple dimensions

- Lower the cost of IT with shared services, and align resources with business demand

- Get a clear picture of your organization’s cost drivers

2020 Redesign to Support the Demands of Today’s Remote World

The 2020 release of Acorn’s PA5G and AAA products feature a new HTML5, web-based UI that makes it simpler to access Acorn from any location or device without the need to install any software on the client. The UI uses the latest modern web technologies while purposely retaining existing functionality, avoiding the need for re-training.

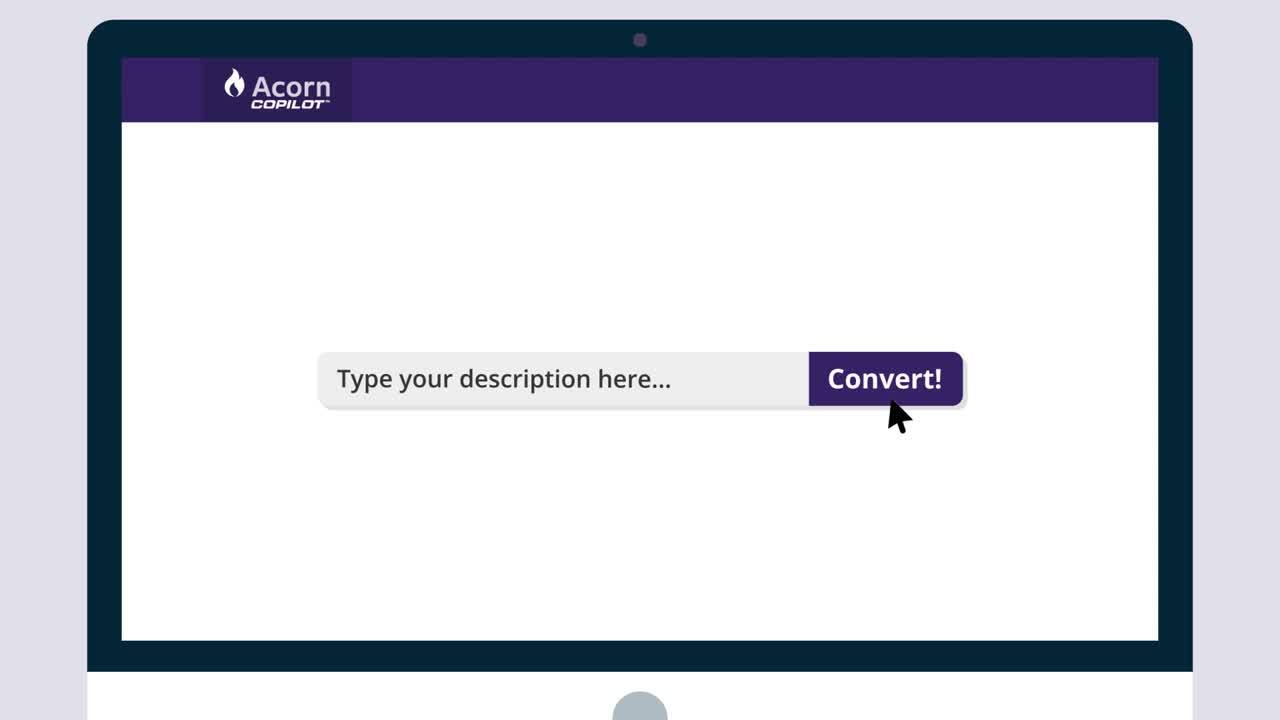

NEW GENAI COPILOT FEATURE

Acorn CoPilot transforms natural language equation descriptions into algorithms written in Acorn's proprietary language. The interactive interface enables field and logic validation, streamlining the equation-building process and saving time.

Natural Language Equation Builder:

What: Converts equation descriptions into Acorn's proprietary language algorithms.

How: Users select a process or driver equation, toggle the "Create Equation from Description" switch, and CoPilot displays the proposed converted equation for approval or edits.

Why: Streamlines the process of creating or editing equations, reducing the time needed to input or change algorithms in the system.

BENEFITS

- Simplified Equation Creation: Save time and effort, especially if you're new to the system.

- Improved User Experience: Create or edit equations easily with an interactive user interface.

COMPLEMENTARY IGNITETECH UNLIMITED SOLUTIONS

Check out the solutions below, available free as part of your Acorn subscription:

Sococo

Sococo

Sococo is the online workplace where distributed teams come to work together each day, side-by-side.

Blog Posts

Apr 17, 2024

IgniteTech Integrates AI Features Across Its Enterprise Software Portfolio

IgniteTech delivers AI-powered enhancements for 12 of its leading software products, available now…

Apr 11, 2024

Supercharge Your Team: Expert Knowledge on Demand with Jive Personas

Discover how Jive Personas, an innovative AI-driven solution, transforms the way organizations…

Apr 8, 2024

How computers understand Human Language

Unravel the mysteries of how computers understand human language through the fascinating world of…

Oct 21, 2020

Announcing IgniteTech Insights, our New ML/AI Offering

New capabilities advance mission-critical Expert System processes

Apr 10, 2019

How Unseen Costs Are Hurting Your Business's Bottom Line

To maintain healthy bottom lines, organizations should consider their options for identifying and…

Jan 4, 2019

Why You Need to Switch to Time-Driven Activity-Based Costing Now

If you haven’t already made the switch to a time-driven ABC model, here’s why you shouldn’t wait any…